The Tax Administration System in China

1.1 In the Mainland, there are 24 types of taxes which are classified under seven categories:

(a) turnover tax (流轉稅),

(b) income tax (所得稅),

(c) resource tax (資源稅),

(d) property and behavior taxes (財產稅及對行為課稅),

(e) agriculture tax (農業稅),

(f) customs tax (關稅), and

(g) tax on prescribed items.

1.2 The legislative and administrative rights of tax laws in the Mainland are vested in various bodies:

(a) The supreme authority to make and interpret tax legislation is vested in the National People’s Congress (全國人民代表大會) and its Standing committee (常務委員會), in accordance with The Constitution of the People’s Republic of China.

(b) As delegated by the National People’s Congress and its Standing Committee, the State Council and State Administration of Taxation can make administrative regulations like ‘regulations’, ‘provisions’, ‘measures’ and ‘detailed rules for implementation’, etc. to administer the tax legislations.

(c) The Provincial People’s Congress (省人民代表大會) and its Standing committee have the right to make local rules and regulations, provided that they do not contravene the Constitution of the People’s Republic of China, or laws made by the National People’s Congress, or the administrative regulations made by the State Council (國務院).

(d) In some large cities, autonomous regions (自治區) and cities where the Special Economic Zones are located, the People’s Government in these locations are also empowered to make provisions and measures.

2. Duties of Tax Bureaus (稅務局)

2.1 Structure of tax authority

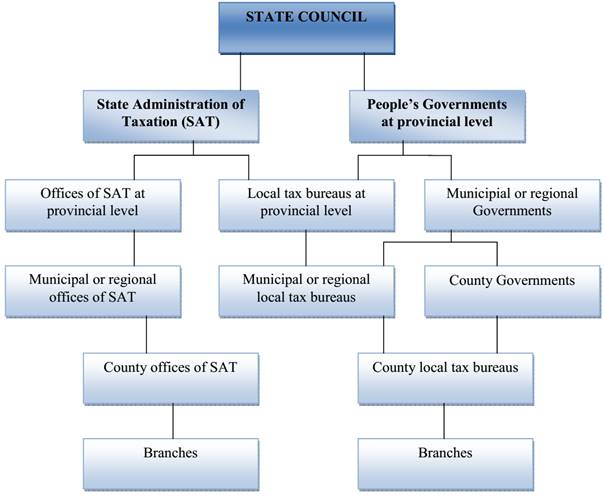

2.1.1 Tax authorities in China are composed of The State Administration of Taxation (SAT) (國家稅務總局), the Ministry of Finance (MOF) (財政部) and local tax authorities.

2.1.2 The SAT is the highest tax authority in China. It is responsible of drafting tax laws, consulting to the State Council on tax policy, formulating implementation procedures and supervising the local tax bureaus which are established as provincial and municipal levels.

2.1.3 The MOF is responsible for formulating implementation procedures and for controlling State budget.

2.1.4

2.2 Tax collection and administration

2.2.1 The state tax authorities are responsible for the administration and collection of taxes that generate revenue for the central government or revenue which is shared between the central and local governments. Major types of taxes collected by the state tax bureaus include VAT, consumption tax, vehicle purchase tax, corporate income tax, etc.

2.2.2 The local tax authorities are responsible for the administration and collection of the taxes that only generate revenue for the respective local governments. Major types of taxes collected by the local tax bureaus include business tax (營業稅), property tax, vehicle and vessel usage tax, stamp duty, deed tax, etc.

3. System for Tax Collection

3.1 System for tax deferral (延期繳稅)

3.1.1 A taxpayer or a withholding agent must hand over the tax payment within the prescribed time limit.

3.1.2 However, a taxpayer under particular difficulties may be allowed to postpone the tax payment for a maximum of three months with the approval of the state tax bureau or local tax bureau of a province, autonomous region and municipality directly under the State Council (Administrative Law on Levying and Collection of Taxes (ALLCT), Art 31).

3.1.3 Such special 'difficulties' may include considerable damage that is caused by force majeure (不可抗力), hence severely affecting the normal production and business activities; insufficient current monetary funds to pay the tax after paying wages owed to employees and social insurances (Regulations on Implementation of Administration of Tax Collection (RIATC), Art 41).

3.2 Surcharge for tax payment

3.2.1 A taxpayer failing to pay tax or a withholding agent failing to deliver the tax payment within the prescribed time limit may be subject to heavy penalties. The taxpayer can be ordered by the tax authorities to pay or hand over the tax before the deadline, and pay a daily surcharge at 0.05% of the tax underpayment counting from the day of deferral (ALLCT, Art 32).

3.2.2 In the event that a taxpayer or a withholding agent has not paid or has underpaid tax owing to a mistake on the part of the tax authorities, the tax authorities may ask the taxpayer or the withholding agent to pay the tax within three years but no surcharge shall be imposed on the underpayment (ALLCT, Art 52).

3.2.3 However, if the failure to levy the tax partially or entirely is caused by fault in calculation or the mistake of the taxpayer, the tax authorities may seek recourse for the tax payment plus a surcharge for the underpayment within three years; and the term for recourse for underpayment may be prolonged to five years in special circumstances.

3.2.4 In addition to the overdue tax surcharge, depending on the reason for non-payment or underpayment of taxes, the tax authorities can impose a non-compliance penalty ranging from 50% to 500% of tax unpaid or underpaid.

3.2.5 Where the under-payment of tax constituted a criminal offence, the taxpayer will be prosecuted for criminal liability in accordance with the relevant laws.

3.2.6 There is no time limit for tax authorities to demand payment of unpaid, underpaid tax and surcharge for overdue tax payment resulting from tax evasion or fraud.

3.3 Tax refunds

3.3.1 Where a taxpayer has overpaid tax, the tax authorities should immediately refund upon discovery of the excess payment.

3.3.2 If the mistake is discovered within three years after the settlement of the tax payment, the taxpayer may make claim to the tax authorities for the excess payment plus the interest at the rate of a bank deposit of the same term (ALLCT, Art 51).

3.3.3 There is no time limitation where the tax authorities discover the overpayment.

4. Tax Disputes and Appeals

4.1 Tax administrative review

4.1.1 Tax administrative review may be instigated by any of the parties (taxpayer, withholding agent or tax payment guarantor). When they believe that the tax specific administrative actions made by tax authorities and their staff infringe upon their legitimate rights and interests, they may make objection by applying to the tax authorities at a higher level or local people's governments for reconsideration in conformity with the law. The department responsible for reconsideration would then make a decision to maintain, change, or revoke the tax specific administrative actions made by the original tax authorities.

4.2 The scope of tax administrative review

4.2.1 'Taxation Administrative Review Regulations' (稅務行政覆議規則) (TARR) [2010] No. 21 ('the Review Regulations') was issued by the State Administration of Taxation on 10 February 2010. The Review Regulations became effective from 1 April 2010.

4.2.2 As specified as under Article 14 of the Review Regulations, the scope of tax administrative review includes the following:

(a) Collection made by tax authority

(i) To collect taxes and add surcharge for tax underpayment

(ii) To withhold and remit tax or collect and remit tax through withholding agents authorised by tax authorities

(b) Order made by tax authority to the taxpayer to provide a guarantee for tax payment.

(c) Measure made by tax authorities to retain tax revenue.

(d) Failure on the part of the tax authorities to lift measures for retaining tax revenue immediately where the legitimate interests of a taxpayer are jeopardised.

(e) Tax mandatory enforcement measures made by tax authority.

(f) Tax administrative penalty made by tax authority.

(g) Failure to handle cases or reply in accordance with law by the tax authority.

(h) Disqualification of Value Added Tax ('VAT') general taxpayers by tax authority.

(i) Notification to the border control authority by the tax authority to prevent taxpayers from departure.

(j) Other specific administrative actions done by tax authorities.

4.3 Tax administrative litigation

4.3.1 In a tax dispute, a taxpayer, withholding agent, or tax payment guarantor should normally pay the tax first including any surcharge for overdue tax payment or provide guarantee in the first place and then apply for tax administrative review.

4.3.2 The taxpayer or the withholding agent may apply to the tax authorities at the superior level for a tax administrative review within 60 days from the date on which the taxpayer was informed of the tax administrative measures taken by its governing tax authority or the date on which the tax and surcharges in disputes were settled or guaranteed.

4.3.3 The superior tax authority should make a decision within 60 days from the acceptance of the review application.

4.3.4 Should the party concerned still not be satisfied, legal proceedings may be instituted with the People's Court (TARR, Article 6). The judge will decide on the legitimacy and justice of the specific tax administrative actions of the tax authority. The scope is basically in line with that of the tax administrative review.

5. Value Added Tax (VAT) (增值稅)

5.1 Scope of VAT

(Dec 14, Jun 15)

5.1.1 VAT is a tax on turnover rather than on profits.

5.1.2 As the name suggests, it is charged on the value added amount. VAT is collected bit by bit along the chain of manufacturing, wholesaling and retailing.

5.1.3 Though VAT is levied on turnover, it is levied only on the value appreciation of every part of the chain in order to avoid double taxation.

5.1.4 Article 1 of the Provisional Regulation on Value-added Tax of the People’s Republic of China (PRVAT) (中華人民共和國增值稅暫行條例), all units and individuals who are engaged in the sales of goods, the provision of processing, repair and replacement services, or the importation of goods, within the PRC territory, are subject to VAT. (在中華人民共和國境內銷售貨物或者提供加工、修理修配勞務以及進口貨物的單位和個人,為增值稅的納稅義務人,應當依照本條例繳納增值稅。)

5.1.5 Units are defined as enterprises, administrative units, public institutions, military units, social organizations and other units.

5.1.6 Individuals are defined widely to include individual business operators and other individuals.

5.2 Deemed sales (視同銷售)

5.2.1 According to Article 3 of the Detailed Rules for the Implementation of the Provisional Regulation on Value-added Tax of the People’s Republic of China (PRVATIR) (中華人民共和國增值稅暫行條例實施細則), the collection of VAT is on the premise of transferring the ownership of goods for compensation.

5.2.2 “Compensation” (有償) in these Detailed Rules includes money, goods, or any economy benefit obtained from the purchaser.

5.2.3 In daily business environment, the following three situations often occur:

(a) transferring goods without transferring property rights;

(b) although changes have been taken place for the property rights of goods, the transfer of goods is not in the form of a direct sale;

(c) the property rights of the goods does not change and the transfer of goods has not yet taken the form of sales, but the goods are used for other purposes similar to sales.

5.2.4 The aforementioned three special circumstances are also subject to VAT. They are called deemed sales, and can be classified into the following categories (PRVATIR, Article 4):

(a) consignment of goods to others;

(b) sales of consigned goods under consignment;

(c) transferring goods from one establishment to another and across cities or counties for sales by a taxpayer who adopts consolidated tax filing;

(設有兩個以上機構並實行統一核算的納稅人,將貨物從一個機構移送其他機構用于銷售,但相關機構設在同一縣(市)的除外)

(d) using self-manufactured goods, or processed goods for non-taxable activities;

(將自産或委托加工的貨物用于非應稅項目)

(e) providing self-manufactured goods, processed goods or purchased goods to other entities or individual business operations as a form of investment;

(f) distributing self-manufactured goods, processed goods or purchased goods to shareholders or investors;

(g) using self-manufactured goods, processed goods for staff welfare or personal consumption;

(h) donating self-manufactured goods, processed goods or purchased goods as free gifts.

Example 1 – Deemed sales |

Company ABC, a general VAT taxpayer, is engaged in car selling. It purchased ten cars in the current month, and obtained VAT special invoice specifying sales value of RMB 800,000 and VAT of RMB 136,000 respectively. In the same month it distributed four of the cars to the shareholders and one car as reward to a salesman. The exclusive price of each car is RMB 130,000. In the above activities, what is the sales amount of the company ABC for VAT purpose? Solution: Distributing purchased goods to shareholders is treated as deemed sales for VAT purpose. Awarding a purchased car to a salesman is also treated as deemed sales (i.e. using purchased goods for employee welfare) for VAT purpose. Thus, the relevant input VAT is not VAT creditable. Then the sales amount of company for VAT is: RMB 130,000 × (4 + 1) = RMB 650,000. |

5.3 Mixed transactions (混合銷售行為)

5.3.1 An economic activity that involves sales of goods as well as the provision of non-taxable labour services is referred to 'mixed transactions'. (一項銷售行為如果既涉及貨物又涉及非應稅勞務,為混合銷售行為)

5.3.2 In other words, a mixed transaction is a single sales transaction which involves both the supplies of goods, the provision of taxable services for VAT purpose and the provision of non-taxable services for business tax purpose (those services would fall within the scope of charge of business tax).

5.3.3 An entity or an individual is considered to be principally engaged in the production, wholesale or retail of taxable goods as its main business if the annual sales amount from sales of goods and taxable services exceeds 50% of the operator's total annual sales amount while the annual amount from non-taxable services makes up less than 50% (PRVATIR, Article 28).

5.4 Concurrent activities

5.4.1 Concurrent activities have to be distinguished from mixed transactions. In both cases, the taxpayers are involved in the sale of goods (subject to VAT) and supply of non-taxable services (subject to BT).

5.4.2 For mixed transactions, a single business involves both taxable and non-taxable activities, and the two activities are connected to each other and are not separately accounted in the sales amount.

5.4.3 However, for concurrent activities, the two activities do not form a single business. Also, the relevant turnover amount are often accounted separately.

5.4.4 PRVATIR, Article 7 stipulates that a taxpayer engaged in non-taxable services as a sideline shall account for the respective amounts of sales of goods, provision of taxable services and provision of non-taxable services.

5.4.5 Without separate and accurate computations, the tax authority has the power to verify or determine the taxable sales amount for VAT purposes.

5.5 Basic principle of tax computation

(Dec 14)

5.5.1 As mentioned above, VAT is levied only on the value appreciation of every part of the chain in order to avoid double taxation.

5.5.2 The value appreciation can be regarded as price difference, that is the balance of turnover received from providing taxable goods and services deducting the purchase price of the goods and services.

5.5.3 VAT payable and input credit (進項稅抵免)

(Dec 12, Dec 14)

VAT payable = Output VAT – Input VAT (應納稅額=當期銷項稅額-當期進項稅額)

Input VAT = VAT paid on purchases

Input VAT paid on purchases of raw materials, fuels and powers such as electricity, heat and gas, low-value and non-durable equipment can be claimed and set off the output VAT.

Starting from 1 January 2009, input VAT paid on purchase of fixed assets can be creditable to offset the output VAT.

5.5.4 VAT special invoices (增值稅專用發票)

The SAT issued Provisions for the Use of Special Invoices of Value-added Tax (VATIP) to regulate the use of VAT special invoices. VAT is shown on VAT special invoice issued by the merchandiser. This reduces the taxpayers' workload of calculating input VAT greatly and makes tax calculation more accurate.

5.5.5 'VAT special invoice' means the invoice which indicates the selling price and output VAT respectively when issued to the purchasers, and the VAT on the invoice is the output VAT to the sellers but the input VAT to the buyers.

5.6 VAT Taxpayers

5.6.1 Generally, the taxpayers can be classified into two categories, the general taxpayer (一般納稅人) and small-scale taxpayers (小規模納稅人).

5.6.2 The general taxpayers are enterprises or other entities whose annual taxable sales amount exceeds the threshold stipulated for small-scale taxpayers.

5.6.3 Small-scale taxpayers also include those who have unsounded accounting and auditing systems and thus have no ability to render relevant ax information accurately according to the VAT sales and regulations.

5.6.4 Unsounded accounting and auditing system is a system which is incapable of accurately accounting for output VAT, input VAT and VAT payable in accordance with the accounting regulations and requirements of the tax authorities.

5.6.5 |

Small-scale taxpayer |

|

A small-scale taxpayer is: [The term “taxpayer engaged principally in the production of goods or services of taxable services” means that the sales amount of goods produced or taxable services provided by the taxpayers annually accounts for more than 50% of the annual taxable sales amount.] |

5.6.6 |

Special rules |

|

There are special rules for general taxpayers, for example: The following are some special rules for the small-scale taxpayer: |

5.7 VAT tax rate

(Jun 12, Dec 16)

5.7.1 The current tax rate of VAT is divided into three classifications:

(a) lower rate of 13%;

(b) basic rate of 17%; and

(c) zero rate which only applies to export goods.

5.7.2 The standard rate of VAT is 17 percent for general VAT taxpayers. The standard rate of 17 percent is applied to the sale and importation of most goods, the provision of repair, replacement and processing services, as well as the leasing of tangible moveable assets.

5.7.3 The following are the main examples of reduced rates, zero rates and exemptions:

VAT tax rate |

Applications |

1. 3% |

‘Small-scale taxpayers,’ being those without sophisticated business, accounting and auditing systems and whose turnover is below certain thresholds (ranging from RMB 500,000 to RMB 5,000,000 for services which have recently transitioned from BT to VAT). These small-scale taxpayers pay output VAT at 3%, but cannot claim input VAT credits on purchases. The 3% ‘simplified’ VAT rate also applies to certain construction services (meaning that output VAT is paid at 3%, but no input VAT credits can be claimed on purchases). |

2. 5% |

This is the simplified VAT rate applicable to certain real estate transactions, and is effectively a transitional measure applied to certain real estate transactions held as at 1 May 2016. |

3. 6% |

‘Modern services’ (being research and development and technical services, information technology services, cultural and creative services, logistics and ancillary services, certification and consulting services, radio, film and television services), value added telecommunications services (e.g. data based telecommunications), financial and insurance services and ‘lifestyle services’ (being education, healthcare, travel, entertainment, food and beverage, accommodation, citizens daily services and cultural and sports services). |

4. 11% |

Transportation services, postal services, basic telecommunications services (e.g. voice based telecommunications), real estate and construction services (though many real estate and construction transactions are subject to reduced rates of VAT pursuant to transitional or grandfathering rules from 1 May 2016). |

5. 13% |

The sale of food grains and vegetable oils, heating, air conditioning, certain gas supplies, books, newspapers and magazines. |

6. Zero-rated |

Exported goods; certain exported services. |

7. Exempt |

Agricultural products, contraceptive drugs and devices, antique books, certain exported services. |

8. Out of scope of VAT |

Interest income on deposits derived by financial institutions, claims paid by insurers and certain merger and acquisition activities. |

(Source: China Country VAT Essentials Guide 2016, KPMG)

5.7.4 As mentioned in the above table, zero rate is applicable to goods declared to export. The export goods qualify for the zero rate or tax exemption except those restricted from exportation.

5.7.5 The zero rate means the taxpayers have no output tax while exporting goods. This is different from tax exemption. The tax effect is different:

(a) When a taxpayer qualifies for zero rate for its business activities:

Tax payable = sales value × 0% – input VAT = – input VAT

Which shall be refund when goods are exported. Hence, zero rate means ‘tax refund for exportation’.

(b) If the goods are tax-exempt instead of qualifying for zero rate, the output VAT is zero. However, the related input VAT cannot be deductible and refunded.

5.8 Payment of VAT

(a) Timing of tax liability

5.8.1 The timing at which VAT liability arises upon the sales of goods or the provision of taxable labour services is determined by the method of settlement or payment modes as follows:

(a) For selling taxable goods, the tax periods shall be decided according to the following situation:

(i) sales of goods by direct payment – on the date when the sales consideration is received or when documentary evidence of the right to collect the sales consideration is received;

(ii) sales of goods on credit or payment by instalment – on the agreed date of collection of sales consideration according to the written contract;

(iii) sales of goods with payment received in advance – on the date when the goods are delivered;

(iv) sales of goods with settlement through collection with the debtor’s acceptance and entrusts the bank for the collection – on the date when the goods are delivered and the collection procedures are completed.

(b) Taxable goods for self-use – on the date when the goods are delivered to use.

(c) Taxable labour services – on the date when the labour services are provided and the consideration is received, or the documentary evidence of the right to collect the considerations is obtained.

(d) Taxable goods of importation – on the date of declaration of customs entry.

(e) Deemed sales – on the date when the goods are transferred.

(b) Timing of input tax credit

5.8.2 General VAT taxpayers who purchase goods or taxable labour services can apply for input tax credit only when the electronically-produced VAT invoice has been verified by the tax authority within 180 days from the date the invoice is issued.

(c) VAT grouping

5.8.3 The Ministry of Finance and the SAT jointly issued Caishui (財稅) [2012] 84 on 31 December 2012 to set out the VAT grouping framework for which head offices and their branches may be eligible.

5.8.4 In other words, the head office calculates the VAT payable both by itself and its branches. The VAT on a grouped basis is paid by the head office to the SAT at the location where the head office is located.

5.8.5 The SAT issued Caishui [2013] No. 74 on 16 November 2013 to replace Caishui [2012] No. 84. Each branch of a company is generally considered as an independent VAT taxpayer. Nevertheless, with the approvals from the Ministry of Finance and the SAT, a qualified company may consolidate VAT and pay it at the head office level. Hence, a qualified company may offset output VAT from one branch against input VAT from another branch.

6. Consumption Tax (消费税)

6.1 Taxable scope and tax rate

6.1.1 Consumption tax (CT) is one of the most important turnover taxes in China. It is levied on manufacturers and importers of certain consumer goods, mostly luxury goods such as tobacco, liquors, cosmetics, jewellery and so on.

6.1.2 The major legislation governing Consumption Tax includes the Provisional Regulations on Consumption Tax of the People's Republic of China (PRCT) (中華人民共和國消費稅暫行條例) and the Detailed Rules for the Implementation of the Provisional Regulations on Consumption Tax of the People's Republic of China (PRCTIR) (中華人民共和國企業所得稅暫行條例實施細則).

6.1.3 CT can be imposed along with VAT on taxable consumer goods.

6.1.4 CT may be charged on a flat rate or fixed tax basis, depending on the types of taxable consumer goods. Typical tax rates are listed below for your reference. However, the tax rates can change from time to time. Practitioners should check with the tax authority for the latest tax rates.

Table of taxable consumer goods and typical tax rates (figures are effective from 1 May 2009 and for an indication only).

Taxable items |

|

Tax unit |

Tax rate / amount |

I |

Tobacco |

|

|

|

1. Cigarettes |

50,000 cigarettes |

RMB 150 |

|

Cigarettes, category A |

RMB 70 or higher for 200 cigarettes |

56% |

|

Cigarettes, category B |

Less than RMB 70 for 200 cigarettes |

36% |

|

2. Cigars |

|

36% |

|

3. Cut tobacco |

|

30% |

II |

Liquor and alcohol |

|

|

|

1. White spirits made from cereals and potatoes |

|

20% + RMB 0.5 per 500 grams |

|

2. Yellow wine |

Tonnage |

RMB 240 |

|

3. Beer |

Priced RMB 3,000 per ton or higher (the price including packaging and packaging deposit, excluding VAT) |

RMB 250 |

|

|

Price less than RMB 3,000 per ton |

RMB 220 |

|

|

Manufactured by catering business and entertainment industry |

RMB 250 |

|

4. Other alcoholic drinks |

|

10% |

|

5. Alcohol |

|

5% |

III. |

Cosmetics |

|

30% |

IV |

Expensive ornaments, pearls, jewellery and jade |

|

5% or 10% |

V |

Firecrackers and fireworks |

|

15% |

VI |

Petroleum products |

Petrol, naphtha, Solvent oil, Lubricant |

RMB 0.10 per litre |

|

|

Aviation kerosene, fuel oil, diesel oil |

RMB 0.80 per litre |

|

|

Leaded gasoline |

RMB 1.4 per litre |

|

|

White gasoline |

RMB 1.0 per litre |

VII |

Motor vehicle tires |

|

3% |

VIII |

Motor cars |

The rate is determined according to cylinder capacity |

1%, 3%, 5%, 9%, 12%, 25%, 40% |

IX |

Motorcycle |

|

3%, 10% |

X |

Golf balls and golf instruments |

|

10% |

XI |

Luxury watches |

RMB 10,000 or higher per one |

20% |

XII |

Yachts |

|

10% |

XIII |

Disposable wooden chopsticks |

|

5% |

XIV |

Hardwood flooring |

|

5% |

6.2 Consumption tax taxpayers

6.2.1 PRCT Article 1 provides that all units and individuals who manufacture, subcontract the processing of, or import and sell taxable consumer goods are chargeable to CT.

6.2.2 'Units' are broadly defined in Article 2 of PRCTIR to mean 'enterprises, administrative agencies, public service units, military units, social organisations and other units.'

6.2.3 'Individuals' include 'individual business operators as well as other individuals who engage in activities in relation to the taxable consumer goods subject to CT.'

6.2.4 Hence the taxpayers of CT are all entities and individuals who engage in the manufacturing, retailing, processing and importation of taxable consumer goods within the territory of China.

6.3 Calculation of consumption tax liability

(a) Ad valorem fixed rate method

6.3.1 Under the ad valorem fixed rate method, the consumption tax liability is subject to sales amount and the applicable tax rate. The formula is:

Consumption tax liability = Sales amount × Applicable tax rate

(b) Taxable sales amount

6.3.2 'Sales amount' is defined under Article 6 of PRCT as the total consideration and other charges receivable from a purchaser on the sale of taxable consumer goods. (銷售額,為納稅人銷售應稅消費品向購買方收取的全部價款和價外費用。)

6.3.3 'Other charges' is defined in Article 14 of PRCTIR to include other service charges, subsidies, funds, fund raising charges, profit returned, penalties, late fees, interest on deferred payment, damages, charges withheld, advances, packaging fees, rentals of packaging, storage fees, quality charges, freight and loading and unloading charges, and charges of any other nature which are in addition to the price charged but exclude certain items like advance freight and government funds. (所稱價外費用,是指價外向購買方收取的手續費、補貼、基金、集資費、返還利潤、獎勵費、違約金、滯納金、延期付款利息、賠償金、代收款項、代墊款項、包裝費、包裝物租金、儲備費、優質費、運輸裝卸費以及其他各種性質的價外收費。)

(c) Conversion of sales amount from the inclusive amount to exclusive amount

6.3.4 While the taxable consumer good is subject to CT, it is also subject to VAT. Under PRCTIR, the 'sales amount' does not include the VAT collected from the buyers. If the output VAT has not been deducted from the sales amount or VAT-inclusive amount has been collected due to inability to issue VAT invoices, CT can be calculated using the sales amount excluding VAT. The conversion formula is as below:

Sales amount excluding VAT = A ÷ (1 + B)

Where:

A = Sales amount including VAT

B = VAT rate or collection rate

6.3.5 When using the conversion formula, the VAT rate or collection rate should be applied according to the taxpayer's specific circumstances. If the taxpayer of CT is a general taxpayer, VAT rate of 17% or 13% applies; if the taxpayer of CT is a small-scale taxpayer, a collection rate of 3% applies since 1 January 2009.

(c) Import of taxable consumer goods

6.3.6 For the imported taxable consumer goods, CT is calculated based on the composite taxable value of the goods.

Composite taxable value |

= |

Value on which customs duty is paid + customs duty |

(1 – applicable CT rate) |

Example 3 – Calculation of consumption tax liability |

A cosmetics manufacturer is a general taxpayer of VAT. It sold cosmetics products to a shopping mall on 10 August 2009 and issued a special VAT invoice. The sales price (excluding VAT) is RMB 400,000 and the output VAT is RMB 68,000. The manufacturer also sold cosmetics products to another company at a sales price of RMB 58,500 (including VAT), and issued a general invoice on 15 August 2009. Required: Calculate the CT liability on the above businesses of the cosmetics manufacturer in August 2009. Solution: CT rate for cosmetics products is 30%; The taxable sales amount of cosmetics products = RMB [400,000 + 58,500 ÷ (1 + 17%)] = RMB 450,000 CT payable = 450,000 × 30% = RMB 135,000 |

(d) Deduction of consumption tax paid

6.3.7 In order to avoid double taxation, the relevant CT rules and regulations provide that, if the purchased taxable consumer goods and consigned processing taxable consumer goods are used for further production of taxable consumer goods for sales, the CT paid is allowed to be deducted from total the CT liability of the final taxable consumer goods.

6.3.8 When calculating the CT liability of the final taxable consumer goods, the relevant CT tax rules and regulations prescribe that the deduction for tax paid shall be calculated according to the amount used in the production during the relevant assessment period.

6.3.9 The formula for calculating the amount of tax paid as above is:

Deductible tax paid on taxable consumer goods purchased from other sources in the current period

= Deductible Purchase price of taxable consumer goods purchased from other sources in the current period × applicable CT rate

Deductible Purchase price of taxable consumer goods purchased from other sources in the current period

= Purchase price of opening balance of taxable consumer goods purchased externally

+ Purchase price of taxable consumer goods purchased from other sources in the current period

– Purchase price of closing balance of taxable consumer goods purchased from other sources

Example 4 |

For a cigarette manufacturing enterprise, the value of opening balance of cut tobacco purchased externally in March was RMB 200,000. The purchase of cut tobacco in March was valued at RMB 500,000 (excluding VAT) from other sources. The value of closing balance of cut tobacco in March was RMB 100,000. Required: Calculate the deductible CT paid of cut tobacco for March. Solution: The applicable CT rate of cut tobacco is 30%. Deductible purchase price of cut tobacco purchased from other sources in the current period Deductible tax paid on cut tobacco purchased from other sources in the current period |

6.4 Consumption tax abatement (減稅)

6.4.1 To protect the environment and encourage replacement of high polluted vehicles, tax incentives are given for certain low-emission vehicles. For these cases, the CT liability may be lowered by 30%. The calculation formula is:

Tax abatement = CT payable computed at statutory rate × 30%

Tax payable = CT payable computed at statutory rate – Tax abatement

Example 5 |

A car manufacturing enterprise, which is a general taxpayer, produced and sold 300 cars in June at VAT-inclusive price of RMB 175,500 each (the relevant VAT rate is 17%). The applicable CT rate is 9%. The tax authority agreed that the cars produced by the enterprise met the national standard for tax abatement. Required Calculate CT payable of the enterprise for June. Solution CT payable before tax abatement = RMB175,500 ÷ (1 + 17%) × 300 × 9% = RMB 4,050,000 |

6.5 Consumption tax refund

(a) Scope of tax refund for export

6.5.1 Certain taxable consumer goods are qualified for a tax refund. The policies for tax refunds are as follows:

(a) tax exemption and refund (foreign trade entities)

Eligible entities are those who have obtained approval for import and export, including the following:

(i) import and export enterprises who purchase taxable consumer goods and export the goods directly;

(ii) foreign trade enterprises who export taxable consumer goods entrusted (委託) by other foreign trade enterprise.

(b) tax exemption, but no tax refund (manufacturing entities)

Eligible entities are those who have obtained approval for import and export, including the following:

(i) manufacturing enterprises with the power to export its own taxable consumer goods by themselves; or

(ii) manufacturing enterprises entrusting foreign trade enterprise to export taxable consumer goods.

For this kind of export, the exporters shall be exempted from CT according to the actual amount exported, but no CT is refunded.

'Tax exemption' refers to manufacturing enterprise exempted from CT of exportation chain according to the actual amount exported.

'No tax refund' refers to the fact that the exported taxable consumer goods have no CT burden included in the FOB because of having exempted from CT upon export of goods. Therefore, there is no need to refund the CT.

(c) No tax exemption and no tax refund

The relevant entities include: enterprises apart from manufacturer and foreign trade enterprise, especially those general commercial enterprises, are not eligible to enjoy tax exemption and tax refund when they entrust foreign trade enterprise to export taxable consumer goods.

6.6 Payment of consumption tax

(a) Timing of tax liability

6.6.1 The timing of CT liability arising is determined respectively according to account settlement and occurrence time of the transactions.

6.6.2 For selling taxable consumer goods, the tax periods shall be decided by the following conditions:

(a) Sales of goods on credit or payment by instalment – on the agreed date of collection according to the written contract.

(b) Sales of goods with payment received in advance – on the date when the goods are delivered;

(c) Sales of goods with settlement through collection with the debtor's acceptance and entrusts the bank for the collection – on the date when the goods are delivered and the collection procedures are completed;

(d) Sales of goods with other settlement methods – on the date either the sales consideration is received or the documentary evidence to collect the sales consideration is received.

6.6.3 Taxable consumer goods for self-use – on the date when the goods are delivered to use.

6.6.4 Taxable consumer goods processed on consignment – on the date of the delivery of goods by the taxpayer.

6.6.5 Taxable consumer goods of importation – on the date of declaration of customs entry.

(b) Tax periods

6.6.6 According to PRCT, the time period for paying CT shall be 1 day, 3 days, 5 days, 10 days, 15 days, one month, or one quarter. Tax that cannot be assessed in regular periods may be assessed on a transaction-by-transaction basis.

7. Individual Income Tax (個人所得稅)

7.1 Introduction

7.1.1 Chinese nationals and foreign individuals who reside in China or have derived PRC-sourced income are subject to Individual Income Tax (IIT) on their employment income, business income or other personal income. There are 11 categories of taxable income.

7.1.2 The original Individual Income Tax Law (IITL) of the People’s Republic of China came into effect on 1 January 1994 and the Individual Income Tax Implementation Rules (IITIR) was issued on 28 January 1994.

7.1.3 The amended IITL came into effect on 1 September 2011. The amended IITIR was issued on 19 July 2011.

7.2 Tax resident (納稅居民)

7.2.1 A PRC tax resident would be subject to IIT on his/her worldwide income whilst a non-PRC tax resident would be subject to IIT on his/her PRC-sourced income (IITL, Article 1).

7.2.2 A PRC tax resident is an individual who is usually or habitually resides in China due to household registration, family or economic relationship (IITIR, Article 2).

(在中國境內有住所的個人,是指因戶籍、家庭、經濟利益關係而在中國境內習慣性居住的個人。)

7.3 Source of income

7.3.1 Whether an individual would be subject to IIT would depend on the following factors:

(a) Whether he/she is regarded as a PRC tax resident or a non-PRC tax resident

(b) The length of his/her stay in the PRC

(c) Whether he/she holds the position of senior management in a Chinese domestic enterprise

(d) The locality of services rendered by him/her

(e) Whether tax treaty exemption is applicable

7.4 Categories of taxable income

7.4.1 The following eleven categories of income are subject to IIT (IITL, Article 2):

(a) Wages and salaries (i.e. Employment income)

(b) Production and business operation derived by individual entrepreneurs operating small businesses

(c) Income derived by an individual from contracting, subcontracting, leasing or subleasing the operations of an enterprise

(d) Income derived by an individual who acts as an independent contractor

(e) Remuneration from manuscripts

(f) Royalties

(g) Interest, dividends (Note) or bonuses received by an individual from loan credits and equity shares

(h) Rental income from property leasing

(i) Income from sales of properties

(j) Contingency income such as winnings, awards or other 'windfall' income

(k) Other taxable income specified by the Ministry of Finance

7.4.2 Directors’ fees are subject to IIT under the category of ‘Income derived by an individual who acts as an independent contractor’.

7.4.3 Income derived from a partnership or a sole proprietorship is taxed under the category of 'Production and business operation derived by individual entrepreneurs operating small businesses.'

7.4.4 The Ministry of Finance and the SAT issued Caishui [2012] No. 85 which provides a 50% IIT reduction on dividend income earned from listed shares held by individual investors for more than one month but not more than one year, and a 75% IIT reduction on dividend income earned from listed shares held by individual investors for more than one year. Caishui [2012] No. 85 became effective from 1 January 2013.

7.5 Employment income

7.5.1 Out of the eleven categories of taxable income, this section will focus on employment income.

(a) Tax relief for temporary visitors

(Dec 15)

7.5.2 A temporary visitor is an individual who has resided in the PRC, continuously or cumulatively, for a total of 90 days or less during a calendar year (or 183 days or less in the prescribed time period if the respective tax treaty applies).

7.5.3 A temporary visitor is exempt from paying IIT on their employment income unless such income is borne or deemed to be borne by any PRC enterprises or a permanent establishment which the employer has in China.

7.5.4 For the purpose of counting the number of days that an individual is present in the PRC during a calendar year, the day of entry into the PRC and the day of departure from the PRC are each counted as one day presence in the PRC (Guoshuifa (國稅發) (2004) 97, Article 1).

7.5.5 A chief representative or registered representative who holds a position in a representative office in China would not be eligible for the above-mentioned 90-day or 183-day exemption rule as their remuneration is deemed to be borne by the PRC representative office.

(b) Special treatment for HK resident employees

(Jun 14)

7.5.6 Starting from 1 June 2012, Hong Kong (and Macau) resident employees can enjoy a favourable treatment for an elimination of double taxation pursuant to a Public Notice (公告) [2012] No. 16 issued by the PRC SAT. The SAT now accepts the time apportionment of the salary and bonus income on the ‘physical day presence’ basis, which is in line with the apportionment basis adopted by the Hong Kong IRD.

7.5.7 According to Public Notice [2012] No. 16, if any Hong Kong resident employee stays in the PRC for not more than 183 days in any 12-month period under the China-HK DTA, his/her PRC IIT liability will be calculated as follows:

IIT payable =

IIT on full income |

× |

No. of days physically present in PRC in a particular month |

× |

Portion of income borne by PRC |

No. of days in that calendar month |

Full income |

7.5.8 The above special tax treatment is only applicable to Hong Kong tax residents who are employed by a Hong Kong company or who are concurrently employed by both a Hong Kong company and a PRC company.

7.5.9 In other words, if the Hong Kong tax resident employee is employed by a PRC enterprise, this special treatment would not be applicable.

7.5.10 The Guangzhou Local Tax Bureau issued Sui Di Shui Ban Fa [2012] No. 27 on 14 August 2012 confirming that starting from 1 June 2012, a Hong Kong or Macau resident who spends all their working days in China but only spends weekends and holidays outside China can enjoy time apportionment based on actual days spent in China.

7.6 Non-PRC tax residents who live in Mainland for more than 90 days or 183 days but less than one full year

(Dec 15)

7.6.1 Individuals who have resided in the PRC for 365 days in any 12-month period are deemed to have lived in the PRC for ‘one full year’. A ‘temporary absence’ from the PRC of 30 days or less for a single trip or 90 days or less for multiple trips are not counted as non-PRC days (IITIR, Article 3).

(税法第一条第一款所说的在境内居住满一年,是指在一个纳税年度中在中国境内居住365日。临时离境的,不扣减日数。

前款所说的临时离境,是指在一个纳税年度中一次不超过30日或者多次累计不超过90日的离境。)

7.6.2 A non-PRC tax resident who resides in the PRC for more than 90 days in any 12-month period (or 183 days in the prescribed period if the respective tax treaty applies) but less than one full year would be subject to IIT on employment income derived during their ‘actual working days in the PRC’.

7.6.3 If the taxpayer is employed by a PRC enterprise, his/her actual working days in the PRC include public holidays, personal vacation days spent inside or outside the PRC and training days.

7.6.4 If the taxpayer does not hold any position in a Chinese enterprise or is not employed by any Chinese enterprise, his/her actual working days in the PRC include work days in the PRC and those public holidays in the period he/she works in the PRC.

7.7 Non-PRC tax residents who live in the Mainland for more than one full year but less than five years

7.7.1 They would be subject to IIT on their PRC-sourced income plus any non-PRC sourced income which is paid to them by a PRC enterprise.

7.8 Individuals who live in the Mainland for five consecutive full years

7.8.1 Once a non-PRC tax resident resides in the PRC for five consecutive full years, he/she would be subject to IIT on his/her worldwide income in any subsequent years (the sixth year onwards) if he/she lives in the PRC for one full year.

7.8.2 However, if such an individual does not live in the PRC for the full year in any subsequent year, he/she would be subject to IIT only on his/her PRC-sourced income for that year.

7.8.3 If such an individual lives in the PRC for less than 90 days in the subsequent year, the five-year period will be re-calculated from the year in which he/she resides for one full year (Caishuizi (財稅字) (1995) 98).

7.9 Individual income tax calculation

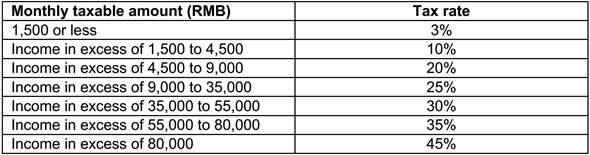

7.9.1 Starting from 1 September 2011, the applicable IIT rate for employment income ranges from 3% to 45% (7 progressive tax brackets), depending on the income level. Please see the tax table below for details.

7.9.2 The prevailing monthly standard deduction for a PRC tax resident and a non-PRC tax resident is RMB3,500 and RMB4,800 respectively.

Tax rate table

Monthly taxable income (with gross-up) |

Monthly taxable income (without gross-up) |

Tax rate |

Quick calculation deduction |

RMB |

RMB |

|

RMB |

Up to 1,455 |

Up to 1,500 |

3% |

0 |

1,456 – 4,155 |

1,501 – 4,500 |

10% |

105 |

4,156 – 7,755 |

4,501 – 9,000 |

20% |

555 |

7,756 – 27,255 |

9,001 – 35,000 |

25% |

1,005 |

27,256 – 41,255 |

35,001 – 55,000 |

30% |

2,755 |

41,256 – 57,505 |

55,001 – 80,000 |

35% |

5,505 |

57,506 and above |

80,001 and above |

45% |

13,505 |

(a) Non gross-up calculations if IIT is paid and borne by the employee

7.9.3 If an employee's IIT liability is paid and borne by himself/herself, the formula for calculating IIT payable on wages and salaries using the quick calculation deduction is as follows:

[Monthly employment income – monthly standard deduction] × applicable tax rate – quick calculation deduction

Example 6 |

Mr. A is a non-PRC tax resident. His monthly employment income is RMB100,000 and he bears his own IIT liability. His IIT liability is calculated as follows: IIT payable = [(RMB100,000 – RMB4,800 (monthly standard deduction)) × 45%] – RMB13,505 = RMB29,335 |

(b) Gross-up calculation if IIT is paid and borne by the employer

7.9.4 If an employee’s IIT liability is paid and borne by his/her employer, the IIT paid should be treated as part of the employee’s remuneration. The employee’s IIT liability should be calculated on a 'gross-up' income as follows:

'Gross-up' taxable income = (A – B – C)/(1 – T)

A = Monthly employment income

B = Monthly standard deduction

C = Quick calculation deduction

T = Applicable tax rate

IIT payable (borne by the employer) = 'Gross-up' taxable income × applicable tax rate – quick calculation deduction

Example 7 |

Using the same information in the above example, if Mr. A’s IIT liability is borne by his employer, his IIT liability is calculated as follows: Gross-up taxable income = (RMB100,000 – RMB4,800 – RMB13,505)/(1 – 45%) = RMB148,536 IIT payable (borne by the employer) = RMB148,536 × 45% - RMB13,505 = RMB53,336 |

Example 8 |

Peter is an expatriate who is stationed to work for a foreign investment enterprise in Shenzhen, the PRC. His monthly salary is RMB20,000. He is responsible for his own IIT liability. Required: Calculate his monthly PRC IIT liability. Solution: Monthly taxable income = RMB (20,000 – 4,800) = RMB 15,200 Progressive tax rates on taxable income from wages and salary (without gross-up) Monthly IIT liability Or |

7.10 Senior management

7.10.1 'Senior management personnel' in a Chinese enterprise is defined in Guoshuihanfa (國稅函發) (1995) 125, Article 3 to include:

(a) General manager

(b) Deputy general manager

(c) Persons assuming functional chief positions

(d) Chief supervisors

(e) Other persons assuming similar company management level positions

7.10.2 Formula to learn

(a) For those who do not spend more than 90 days in a calendar year (or 183 days if the respective tax treaty applies) would be subject to IIT as follows:

Total IIT on salaries from inside and outside the Mainland for a month |

× |

Salary derived or paid in the PRC during the month |

Total salary received during the month |

(b) For those who spend more than 90 days (or 183 days if the respective tax treaty applies) but less than five years would be subject to IIT as follows:

Total IIT on salaries from inside and outside the Mainland for a month |

× |

(1 – time apportionment factor) |

Time apportionment factor

![]()

(c) For those who spend five full consecutive years, they would be subject to IIT on their worldwide income.

7.11 Tax administration

7.11.1 Individuals who are liable to IIT should be required to register with the local tax bureau. The tax registration requirements may vary depending on the requirements of the local tax bureau.

7.11.2 Generally speaking, the employer (i.e. the payer of employment income) should act as the withholding agent to withhold IIT from wages and salaries payable to employees on a monthly basis.

7.11.3 An individual taxpayer with annual taxable income (from all eleven categories) of more than RMB120,000 per annum would be required to self-report his/her taxable income to the local tax bureau in-charge within three months after the year end (IITIR, Article 36).

7.11.4 IIT on wages and salaries is calculated and levied on a monthly basis. Withholding agents should submit IIT withholding returns and make the related tax payments to the local tax bureau in-charge within 15 days after the end of the month.

8. Corporate Income Tax (企業所得稅)

8.1 Tax resident

8.1.1 Starting from 1 January 2008, all enterprises including foreign investment enterprises, foreign enterprises and Chinese domestic enterprises which derive income within the territory of the PRC shall be liable to Corporate Income Tax (CIT).

8.1.2 The prevailing CIT Law (CITL) was promulgated on 16 March 2007 which unifies the income tax treatments of domestic and foreign investment enterprises. The CITL became effective on 1 January 2008. The CIT Law Implementation Rules (CITIR) were issued on 11 December 2007.

8.1.3 A PRC tax resident would be subject to CIT on its worldwide income whilst a non-PRC tax resident would be subject to CIT on its PRC-sourced income.

8.1.4 A PRC tax resident includes an enterprise which is established in the PRC pursuant to Chinese laws OR an enterprise which is established under the laws of a foreign country but has ‘effective management’ in the PRC. (CITL, Article 2)

8.1.5 The CITIR defines the ‘place of effective management’ as the place where the overall management and control of the production and business operations, personnel, accounting, properties etc is exercised.

8.1.6 A non-PRC tax resident refers to an enterprise established under the laws of a foreign country and has its place of effective management outside the PRC but with an 'establishment' in the PRC.

8.1.7 A non-PRC tax resident also includes a foreign company which does not have an ‘establishment’ in the PRC but derives PRC-sourced income. (CITL, Article 2).

8.1.8 Establishment are defined under Article 5 of CITIR to include:

(a) a place of management or operation;

(b) a farm, factory or place of extraction of natural resources;

(c) a place where services are rendered;

(d) a place of construction, installation, assembly, repair and exploration; and

(e) other establishments engaged in manufacturing and business operating activities.

8.2 Corporate income tax computation

(a) PRC tax residents

8.2.1 CIT is levied at a rate of 25% on the taxpayer’s net taxable income on an annual basis. The taxpayer’s net taxable income in a tax year (1 January to 31 December of every year) is calculated after deducting the non-taxable items, tax-exempt items, other allowable items and the agreed tax losses carried forward from its incomes (CITL, Article 5).

8.2.2 The State-encouraged High-and-New Technology Enterprises (國家重點扶持的高新技術企業) are subject to a reduced CIT rate of 15% (CITL, Article 28).

8.2.3 Small-scale enterprises are subject to a reduced CIT rate of 20% (CITL, Article 28). Small-scale enterprises include:

(a) industrial enterprises whose annual taxable income does not exceed RMB300,000, the number of employees does not exceed 100 and the total assets do not exceed RMB30 million.

(b) non-industrial enterprises whose annual taxable income does not exceed RMB300,000, the number of employees does not exceed 80 and the total assets do not exceed RMB10 million (CITIR, Article 92).

8.2.4 In calculating the CIT, some items have deduction thresholds. For example,

(a) the deduction threshold of employee’s welfare expenses, employee’s education expenses and labour union fees are 14%, 2.5% and 2% respectively of the wages and salaries paid in a tax year.

(b) Entertainment expenses incurred in relation to the production and business operation are deductible to the extent of 60% of the entertainment expenses incurred, but subject to a cap of 0.5% of total revenue of a tax year.

(c) An enterprise may claim qualified donations of up to 12% of its annual profit as deductible expenses (CITL, Article 9).

8.2.5 Advertising and promotional expenses will be deductible up to 15% of annual sales revenue for corporate income tax purposes. This cap can be increased to 30% of annual sales revenue for manufacturing companies of cosmetics, pharmaceutical products and non-alcoholic beverages as well as trading companies of cosmetics up until 31 December 2015 (Caishui [2012] No. 48).

8.2.6 On 29 September 2013, the Ministry of Finance and the SAT jointly issued Caishui [2013] No. 70 to expand the scope of research and development expenses that are eligible for super deduction (150% of the actual expenses) for corporate income tax purposes. Caishui [2013] No. 70 took effect on 1 January 2013.

8.2.7 Depreciation can be computed using the straight line method. According to article 59 of CITIR, no more fixed residual percentage is required. The minimum depreciation period ranges from 3 years for electronic equipment to 20 years for building.

8.2.8 The Ministry of Finance and the SAT have jointly issued Caishui [2014] No. 75 in September 2014. Caishui [2014] No. 75 expands the scope of fixed assets to which accelerated depreciation methods for CIT deduction purpose can be applied. Caishui [2014] No. 75 became effective retrospectively from 1 January 2014.

8.2.9 Tax losses incurred by enterprises in a tax year can be carried forward to set off against taxable profits of the next five years (CITL, Article 8). Tax losses cannot be carried backward.

8.2.10 Companies established in Shenzhen Qianhai Modern Services Industry Cooperation Zone (前海深港現代服務業合作區), Hengqin New Area (橫琴新區) and Pingtan Comprehensive Experimental Zone (平潭綜合實驗區) which are engaged in Qualified Encouraged Industries may enjoy a reduced CIT rate of 15%. Caishui [2014] No. 26 issued by the Ministry of Finance and the SAT on 27 March 2014 clarifies the policies and conditions that need to be fulfilled.

8.3 Non-PRC tax residents with establishments in the Mainland

8.3.1 Non-resident enterprises with establishments in the PRC would pay CIT on PRC-sourced income and income which is 'effectively connected' with its establishments in the PRC (CITL, Article 3).

8.3.2 The 'effectively connected income' (實際聯繫的所得) refers to income earned by the establishments of the non-PRC tax resident.

8.3.3 According to Guoshuifa (2010) No.19, non-resident enterprises which have establishments in the PRC should set up accounting books in accordance with the Tax Collection and Administration Law and maintain adequate accounting records so as to calculate the taxable income.

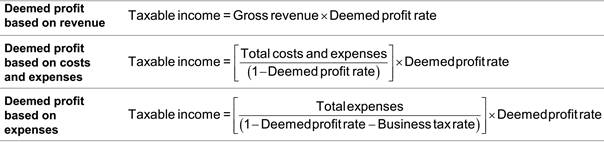

8.3.4 If a non PRC tax resident is unable to accurately calculate its taxable income because of incomplete accounting records or a lack of information, the PRC tax authorities are empowered to assess the taxable income based on one of the following methods (Guoshuifa (2010) No. 19, Article 4):

8.3.5 According to article 5 of Guoshuifa (2010) No. 19, the deemed profit rate of a non-resident enterprise is determined by the local tax bureau in-charge. The general guidelines are as follows:

Provision of construction, design and related consulting services |

15% to 30% |

Provision of management services |

30% to 50% |

Provision of other services |

Not less than 15% |

8.4 Non-PRC tax residents without any establishments in the Mainland

8.4.1 A non-PRC tax resident which does not have any establishment in the PRC may derive PRC sourced income (e.g. dividends, interest, royalties, rental income and gains from the transfer of assets). Such non-PRC tax resident would normally be subject to withholding tax on the gross income.

8.4.2 The applicable withholding tax rate is 10% (CITIR, Article 91). The applicable withholding tax rate may be reduced under the respective tax treaties between the Chinese government and the overseas jurisdictions provided that certain conditions are satisfied.

8.4.3 According to CITL and CITIR, BT paid on interest or royalty income is not deductible in calculating the withholding tax liabilities. (CITL, Article 19; CITIR, Article 103).

8.5 Tax administration

(a) Provisional filing obligation

8.5.1 These enterprises should file quarterly provisional CIT returns to the local tax bureau in-charge within 15 days after the end of each quarter and make the corresponding tax payments (CITL, Article 54).

8.5.2 The provisional tax payments can be calculated based on actual profits of a quarter or quarterly taxable income of the previous tax year.

8.5.3 Regardless of whether an enterprise incurs taxable profits or losses in a tax year, such an enterprise is required to file provisional CIT returns (CITIR, Article 129).

(b) Annual filing obligation

8.5.4 These enterprises should also submit annual CIT returns and settle the final tax payments within 5 months after the end of each tax year (1 January to 31 December).

8.5.5 Audited financial statements should be submitted together with the annual CIT returns.

8.5.6 Provisional quarterly CIT paid can be used to set off the annual CIT liability. Any CIT overpayment can be refunded.

8.5.7 Regardless of whether an enterprise incurs profits or losses in a tax year, such enterprise is required to file its annual CIT return and audited financial statements to the PRC tax bureau (CITIR, Article 129).

(c) Non-PRC tax residents without any establishments in the Mainland

8.5.8 The payer (who made payments to the non-resident recipients) shall be the withholding agent (CITL, Article 37). The withholding agent is required to withhold the tax liability from each payment made to the non-resident taxpayer upon the time of actual payment or when the payable amount is due or payable (CITL, Article 37).

8.5.9 An amount is due or payable when such payable item is booked by the payer as a cost or expense on an accrual basis (CITIR, Article 105). When the payer (e.g. a PRC enterprise) has already recorded the payments as costs or expenses and claimed deductions for those expenses in their CIT returns, the payer should withhold the relevant CIT before making the payment to the nonresident recipients.

8.5.10 A tax withholding agent is required to perform the tax withholding registration to the local tax bureau in-charge within 30 days from the commencement of withholding obligations (Regulations on Implementation of Administration of Tax Collection, Article 13).

8.5.11 The withholding agent is obliged to withhold tax from payments of dividends, interest, royalties, rental etc. within seven days of each payment.

Example 2 – VAT computation |

||||||||||||||||||||

A manufacturer has 2 production chains: The first one is to process material A into product B, and the second one is to continuously process product B into product C. The following purchase price and selling price are VAT exclusive and the applicable VAT rate is 17%:

The first chain: The manufacturer bought material A for manufacturing and sell product B later. It paid VAT of RMB 17 to the suppliers (i.e. input VAT (進項增值稅)) in addition to the purchase price of RMB 100. Therefore, the total payment was RMB 117. When product B was sold, its customer was charged RMB 234, of which RMB 200 was the selling price and RMB 34 was the VAT (i.e. output VAT (銷項增值稅)). In sum, the VAT payable of this chain is calculated as follows: VAT payable = Appreciation value × Applicable tax rate = RMB 100 × 17% = RMB 17, or The second chain: We assume that the manufacturer is a general taxpayer for VAT purposes in the above example. |

Source: https://hkiaatevening.yolasite.com/resources/QPMDNotes/Ch20-ChinaTax.doc

Web site to visit: https://hkiaatevening.yolasite.com/r

Author of the text: Prepared by Harris Lui Copyright @ HKSC 2017

If you are the author of the text above and you not agree to share your knowledge for teaching, research, scholarship (for fair use as indicated in the United States copyrigh low) please send us an e-mail and we will remove your text quickly. Fair use is a limitation and exception to the exclusive right granted by copyright law to the author of a creative work. In United States copyright law, fair use is a doctrine that permits limited use of copyrighted material without acquiring permission from the rights holders. Examples of fair use include commentary, search engines, criticism, news reporting, research, teaching, library archiving and scholarship. It provides for the legal, unlicensed citation or incorporation of copyrighted material in another author's work under a four-factor balancing test. (source: http://en.wikipedia.org/wiki/Fair_use)

The information of medicine and health contained in the site are of a general nature and purpose which is purely informative and for this reason may not replace in any case, the council of a doctor or a qualified entity legally to the profession.

The texts are the property of their respective authors and we thank them for giving us the opportunity to share for free to students, teachers and users of the Web their texts will used only for illustrative educational and scientific purposes only.

All the information in our site are given for nonprofit educational purposes