Chapter 14 Audit of Cash and Bank Balances

LEARNING OBJECTIVES 1. Understand the internal controls over custody of cash. |

1. Importance and Assertions for the Audit of Cash and Bank Balances

1.1 Importance of the audit of cash and bank balances (Pilot, Jun 13)

1.1.1 The audit of cash is considered an important part of an audit mainly due to two reasons:

(a) Almost all business transactions will be ultimately settled through the cash accounts, the audit of cash accounts also assists in the verification of other asset and liability accounts as well as revenue and expenses.

(b) Cash is the highly liquid asset in a company and it is an area of high inherent risk since there is a relatively high risk of misappropriation.

1.2 Assertions for auditing cash and bank balances (Pilot)

1.2.1 The assertions for auditing cash and bank balances are as follows:

Assertions |

Descriptions |

1. Existence |

|

2. Completeness |

|

3. Accuracy |

|

4. Cut-off |

|

5. Presentation and disclosure |

|

6. Detail tie-in |

|

2. Internal Controls for Cash and Bank Balances

2.1 Inherent risks

2.1.1 Unless the client’s business is a retail business which involves significant amount of cash balances daily, the cash balance is usually immaterial in most audit.

2.1.2 From a good internal control point of view, an imprest petty cash fund is usually maintained. It is operated by established a fixed amount of petty cash fund transferred from the business’s general cash in bank account.

2.1.3 Cash is more susceptible to theft; therefore, there is high inherent risk for the existence, completeness, and accuracy objectives.

2.1.4 Internal control objectives for cash:

Control objectives |

Description |

Existence |

(i) Division of duties among custody, recording, authorization and replenishing petty cash fund. |

Completeness |

(i) Prenumbered petty cash vouchers should be used for withdrawing cash from the fund and a limit should be placed on the size of reimbursements. |

2.1.5 Control activities for cheque receipts: (Jun 14)

(a) Segregation of duties in the handling of cheque receipts and recording.

(b) Immediate preparation of incoming cheque listing and endorsement of incoming cheques.

(c) Timely deposit of cheques, preferably on a daily basis.

(d) Cash receipt journal vouchers prepared from cheque listing an pay-in slips and approved by senior accounting staff before input into cash book.

(e) Periodic bank reconciliations prepared by an independent accounting staff members.

(f) Independent review of bank reconciliation.

3. Substantive Procedures

3.1 Analytical procedures

3.1.1 Since cash does not have a predictable relationship with other financial statement accounts because of its residual nature, therefore, the auditor’s use of analytical procedures for auditing cash balances is limited to:

(a) Compare with prior years’ cash balances and to budgeted amount.

(b) Identify receipts of the next accounting period and investigate the long outstanding cheques, determine whether they should be reflected in the balances at year end period.

3.2 Substantive procedures of cash receipts and payments transactions

3.2.1 The substantive procedures:

Audit Objectives |

Substantive Procedures |

1. Occurrence / Existence |

|

2. Completeness |

|

3. Accuracy |

|

4. Valuation |

|

5. Cut-off |

|

6. Classification |

|

3.3 Test of details of cash balances

3.3.1 The substantive procedures for test of details of cash balances

Audit Objectives |

Substantive Procedures |

1. Occurrence, completeness and valuation |

|

2. Accuracy |

|

3. Cut-off |

|

4. Classification, presentation and disclosure |

|

4. Bank Reconciliation

4.1 Audit procedure of testing bank reconciliation (Pilot, Jun 10, Jun 13, Jun 14)

(a) Test the mathematical accuracy of the bank reconciliation and agree the balance in the cash book.

(b) Agree the bank balance on the bank reconciliation with the balance on bank confirmation.

(c) Trace the deposits in transit on the bank reconciliation to the cut-off bank statement covering a week after the date on which the bank account is reconciled.

(d) Agree any charges included on the bank statement to the bank reconciliation.

(e) Agree the adjusted book balance on the cash account lead schedule.

(f) Trace bank transfers for last week of financial year under review and first week of the following year for proper cut-off.

(g) Identify irregular items and obtain necessary explanation.

5. Bank Confirmation

5.1 Importance of bank confirmation

(Pilot)

5.1.1 The sending of bank confirmation is important to auditing of cash for the following reasons:

(a) Direct confirmation of bank balances gives the auditor independent, third-party evidence.

(b) The bank letter may reveal details of security, borrowings and contingent liabilities which need to be disclosed in the financial statements.

(c) Information obtained from bank confirmation requests assists the auditor in discharging his responsibilities to obtain sufficient appropriate audit evidence by providing external evidence in relation to such matters as the existence, completeness and valuation of assets and liabilities.

(d) The auditor may need to carry out additional tests on matters after reviewing the replies from banks.

5.2 Sending bank confirmation

5.2.1 When the auditor determines to send bank confirmation, the following matters should be considered:

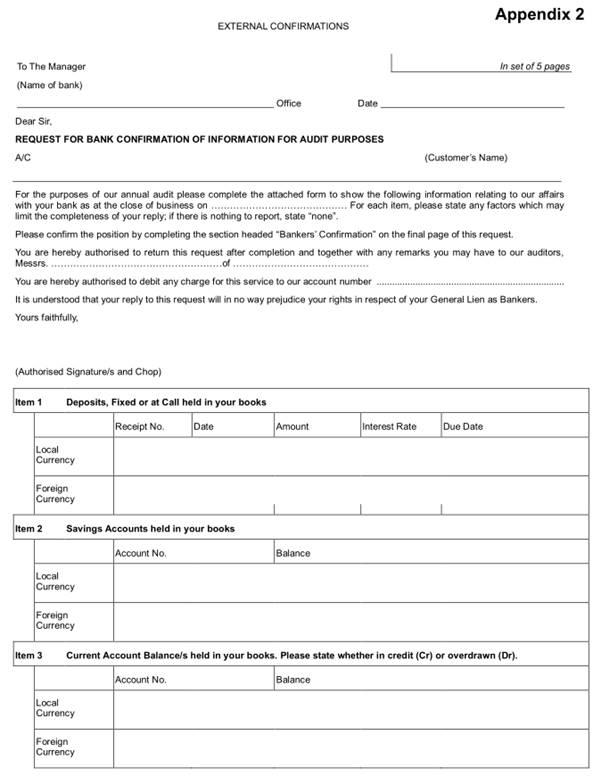

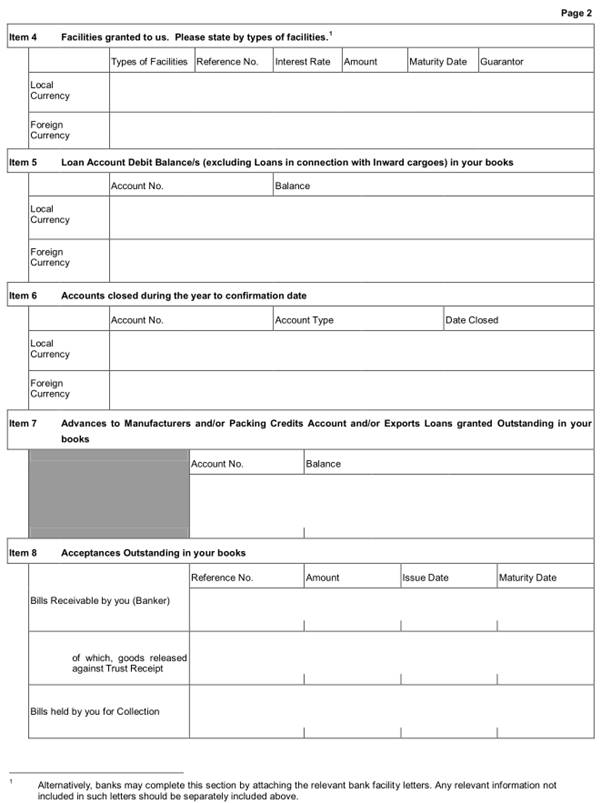

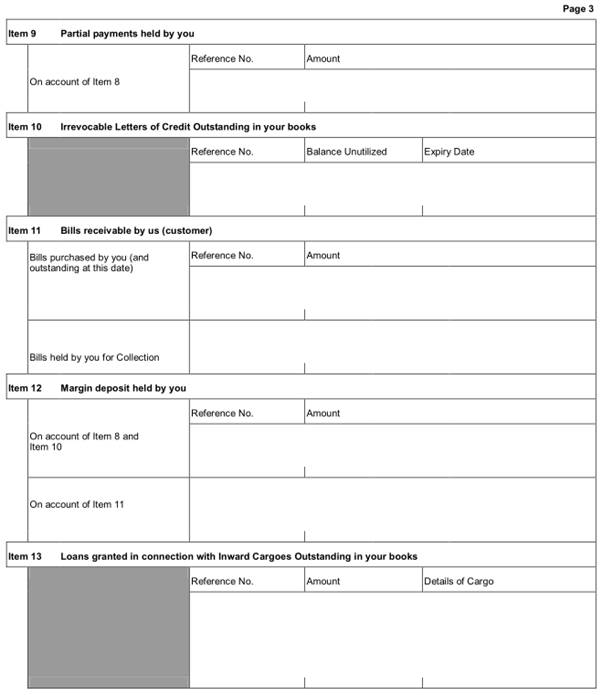

(a) The format of the letter is usually standard and agreed between the banking and auditing professions (HKSA 505 (Clarified) External Confirmations, Appendix 2: Standard Bank Confirmation Request Form).

(b) Ensure that all banks that the client deals with are circularized.

(c) The entity is to complete and sign the authorization on the bank confirmation request, requesting its completion by the bank and then directly return to the auditor.

(d) The balance for each bank account should be agreed to the following items:

(i) bank reconciliation

(ii) interest charges to interest expense account in the general ledger

(iii) details of loans to the disclosure in the statement of financial position to ensure it is correctly classified into the current and non-current elements

(e) If the bank does not respond to a confirmation request, the auditor should send a second request or ask the client to remind the bank on this matter.

Question 1 Required: (a) The balance of cash account is relatively small compared to the balances of other assets. Why is the audit of cash an important part of the audit? (4 marks) Evaluate this statement by considering the circumstances under which evidence gathered is in general considered to be reliable in accordance with HKSA 500 Audit Evidence. (5 marks) |

6. Fraud-Related Audit Procedures

6.1 When the auditor assesses the client’s control over cash is weak and suspects that some type of fraud or defalcation involving cash has occurred, the following audit procedures are typically used to detect fraudulent activities in the cash accounts:

(a) Proof of cash

(b) Testing for kiting (補空)

(c) Testing for lapping

6.2 Proof of cash

6.2.1 A proof of cash is used to reconcile the cash receipts and disbursements recorded on the client’s books with the cash deposited into and disbursed from the client’s bank account for a specific time period. The purposes of the proof of cash are to ensure:

(a) All cash receipts recorded in the client’s accounting records were deposited in the client’s bank account.

(b) All cash payments recorded in the client’s accounting records have been cleared.

(c) No bank transactions have been omitted from the client’s accounting records.

6.2.2 However, a proof of cash cannot detect a theft of cash when the cash was stolen before being recorded in the client’s books. If the auditor suspects that cash was stolen before being recorded in the client’s books, the audit procedures for testing the completeness in recording cash receipt transactions should be performed.

6.3 Test of kiting

6.3.1 When cash has been stolen by an employee, he can conceal the cash shortage by means of kiting. This involves an employee covering the cash shortage by transferring money from one bank account to another and recording the transactions improperly on the client’s books.

6.3.2 The cash shortage can be covered up by preparing a cheque on one account just before year end; however, this transaction is not recorded until the next period. The cheque is deposited in a second account just before year-end and recorded as a cash receipt in the current period.

6.3.3 Kiting is detected by preparing an interbank transfer schedule. Interbank transfer schedule is usually obtained if there are numerous bank transfers, regardless of internal controls or for the purpose of detecting suspected fraud.

6.3.4 Audit procedures that should be done on interbank transfer schedule are as follows:

(a) Verify the accuracy of the information by comparing the disbursements and receipts to cash book.

(b) Compare the dates of transfers on the schedule with the bank statement, noting that all transfer a few days before and after the end of the reporting period has been included on the schedule.

6.3.5 |

Example 1 |

|||||||||||||||||||||||||||||||||||

|

Which of the following cash transfers results in a misstatement of cash at 31 December 2007?

Ans: B is correct because the receipt is recorded on the books prior to year-end, while the disbursement is recorded subsequent to year-end. Therefore, the cash on the books is overstated. |

|||||||||||||||||||||||||||||||||||

6.4 Test for lapping

6.4.1 Additional procedures can be performed to try to detect attempts at lapping accounts receivable collections include:

(a) Obtaining a cut-off bank statement and checking the proper listing of outstanding cheques and deposits in transit on bank reconciliation.

(b) Checking the details of customer payments listed in bank deposits in comparison to details of customer payment in daily remittance list or other record of detail postings.

(c) Comparing the cheques listed on a sample of deposit slips from the reconciliation month to the detail of customer credits listed on the day’s posting to customer accounts receivable.

HKSA 505 “External Confirmations” – Bank Confirmation

Source: https://hkiaatevening.yolasite.com/resources/PBEAuditNotes/Ch14-CashBank.doc

Web site to visit: https://hkiaatevening.yolasite.com

Author of the text: indicated on the source document of the above text

If you are the author of the text above and you not agree to share your knowledge for teaching, research, scholarship (for fair use as indicated in the United States copyrigh low) please send us an e-mail and we will remove your text quickly. Fair use is a limitation and exception to the exclusive right granted by copyright law to the author of a creative work. In United States copyright law, fair use is a doctrine that permits limited use of copyrighted material without acquiring permission from the rights holders. Examples of fair use include commentary, search engines, criticism, news reporting, research, teaching, library archiving and scholarship. It provides for the legal, unlicensed citation or incorporation of copyrighted material in another author's work under a four-factor balancing test. (source: http://en.wikipedia.org/wiki/Fair_use)

The information of medicine and health contained in the site are of a general nature and purpose which is purely informative and for this reason may not replace in any case, the council of a doctor or a qualified entity legally to the profession.

The texts are the property of their respective authors and we thank them for giving us the opportunity to share for free to students, teachers and users of the Web their texts will used only for illustrative educational and scientific purposes only.

All the information in our site are given for nonprofit educational purposes