Introduction to Treasury Management

1.1 |

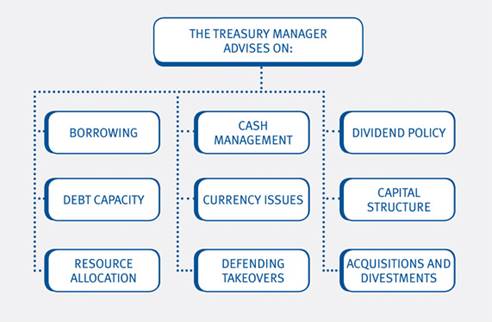

Treasury function |

|

The treasury function is responsible for the following areas: |

1.2 The stability of the company’s cash flows to achieve the company’s profit and solvency objectives is the key aim of treasury.

2. The Structure of the Treasury Function

2.1 Treasury activities

2.1.1 Treasury tends to concentrate on the physical flow of funds, cash and financial risk as compared to accounting and corporate finance, which deal predominantly with the recording or evaluation of transactions. In general, treasury usually adopts a more active role in the organisation than other sections of the finance function.

2.1.2 Originally the activities were carried out within the general finance function, but today are often separated into a treasury department, particularly in large international companies. Reasons for the change include:

(a) increase in size and global coverage of the companies

(b) increasingly international markets

(c) increase in sophistication of business practices.

2.2 Centralisation of the treasury department

2.2.1 The following are advantages of having a specialist centralized treasury department.

(a) Centralised liquidity management

(i) Avoid having mix of cash surpluses and overdrafts in different localized bank accounts.

(ii) Facilitates bulk cash flows, so that lower bank charges can be negotiated.

(b) Larger volumes of cash are available to invest, giving better short-term investment opportunities (for example money markets, high-interest accounts and CDs).

(c) Any borrowing can be arranged in bulk, at lower interest rates than for smaller borrowings, and perhaps on the eurocurrency or eurobond markets.

(d) Foreign exchange risk management is likely to be improved in a group of companies. A central treasury department can match foreign currency income earned by one subsidiary with expenditure in the same currency by another subsidiary. In this way, the risk of losses on adverse exchange rate movements can be avoided without the expense of forward exchange contracts or other hedging methods.

(e) A specialist treasury department can employ experts with knowledge of dealing in forward contracts, futures, options Eurocurrency markets, swaps, and so on. Localised departments could not have such expertise.

(f) The centralized pool of funds required for precautionary purposes will be smaller than the sum of separate precautionary balances which would need to be held under decentralized treasury arrangements.

(g) Through having a separate profit centre, attention will be focused on the contribution to group profit performance that can be achieved by good cash, funding, investment and foreign currency management.

2.3 Decentralization of treasury department

2.3.1 Possible advantages of decentralized cash management are as follows.

(a) Sources of finance can be diversified and can match local assets.

(b) Greater autonomy can be given to subsidiaries and divisions because of the closer relationships they will have with the decentralized cash management function.

(c) A decentralized treasury function may be more responsive to the needs of individual operating units.

3. Cost Centre or Profit Centre

3.1 Treasury department as a cost centre

3.1.1 If the treasury function is established as a cost centre, the costs of the department can be charged to the various other departments/subsidiaries on some basis that is seen to fairly reflect the benefits the other department/subsidiary obtains from the treasury department and the use it makes of the treasury services.

3.1.2 If it is not possible to allocate costs on a basis that is seen to be fair, the company may simply treat the costs as a head office expense.

3.2 Treasury department as a profit centre

3.2.1 Alternatively, the treasury function could be established as a profit centre if revenues arising from treasury can be identified. Revenues could be recognised as follows:

(a) Treasury could charge all other departments/subsidiaries and other head office departments a fee for its services based on current market rates (the total value charged to the group as a whole should exceed the treasury's costs enabling it to report a profit).

(b) Treasury could also earn a profit through its management of the group's exposure to interest rate and foreign exchange risk. Specialists at the treasury department may decide not to hedge group exposure to these risks in certain circumstances. If interest rates or exchange rates subsequently move in the company's favour the benefits could be credited to the treasury department. On the other hand, if such decisions resulted in subsequent losses these would be charged to treasury.

(c) Deciding not to hedge all currency and interest rate risks. Experts in the treasury could decide which risks not to hedge, hoping to profit from un-hedged favourable exchange rate and interest rate movements.

(d) If the treasury department decided to take on additional exchange rate or other risks purely as a speculative activity (for example, writing options on currencies or on shares held) the profits or losses from these transactions could be credited or debited to the treasury function. The board must specify the policy framework within which such speculative trades are carried out and stringent procedures would need to be in place to ensure that these guidelines are adhered to.

3.3 Advantages of profit centre

3.3.1 The following advantages may result from establishing the treasury function as a profit centre:

(a) Treasury function may be able to make a significant contribution to group profit through undertaking some of the actions described above.

(b) Motivation of the specialists employed in treasury may be improved, as they will now be assessed in terms of their contribution to group profit (as compared with the situation if treasury is treated as a cost centre and its costs are simply allocated throughout the group).

3.4 Disadvantages of profit centre

3.4.1 The disadvantages of establishing a separate treasury department as a profit centre are as follows:

(a) The group will incur additional administrative cost if it has to collect data on the revenues of the treasury function as well as its costs.

(b) Problems are likely to arise in establishing a satisfactory charge for treasury's services to other departments/subsidiaries.

(c) The risks of speculation. In practice, many treasury functions have run into difficulties speculating in derivative products and then have tried to trade their way out of the problem. The result has been some disastrous and well-publicised losses. If the group treasury function is to be allowed to engage in such speculative trades it must be closely supervised by trained management to ensure that risk exposure limits are not exceeded.

4. Treasury Policies Required Board Level Approval

4.1 Financial policy

4.1.1 Financial policy should address gearing and maturity issues, fixed and variable interest rate obligations, foreign exchange risk management, dividend policy and covenants. The company requires as much operational and financial flexibility as possible.

4.2 Funding policy

4.2.1 The board should have regular, informed discussions about funding possibilities to put currency, maturity, cost and equity/debt character into a wider context.

4.2.2 This lets the board delegate fund raising decisions and actions to treasury. Treasury, however, must still have final board approval for:

(a) the types of instruments that may be used in debt, investment and risk management

(b) their use, and under what conditions they may be used.

4.3 Banking

4.3.1 Banks chosen by the treasurer must be able to meet the needs of the organisation, both domestically and internationally. The board should approve the organisation's list of bankers annually while resisting the temptation to interfere in the relationships.

4.4 Liquidity

4.4.1 The board must approve of commercial paper programmes. The board should also approve treasury's policy on the investment of surplus funds, the choice of instruments, the list of institutions used, the maximum amount and maturity that can be placed with one counterparty, any hedging, swaps and other financial instrument arrangements entered into.

4.5 Foreign exchange

4.5.1 Treasury policies in this area must be clearly explained to and understood by the board. Treasury must alert the board to external changes and internal strategic developments, which may have long-term implications for the organisation and to make proposals for managing them. The board must approve the hedging policy, the company's foreign exchange management philosophy and its attitude to risk.

4.6 Interest rate hedging policy

4.6.1 Managing interest rate exposure requires a forward projection to be taken of the prospective future movements in interest rates. The board should fully consider the risks involved in the company's activities and develop a level of awareness among senior management of possible unexpected losses that may result from adverse movements in interest rates.

4.6.2 An explicit board policy is ideal. From the board's viewpoint, staff are made aware of its philosophy and objectives and are provided with the working guidelines to achieve those objectives.

4.7 Instruments and techniques

4.7.1 In all areas of funding and liquidity, foreign exchange, interest and commodity price risk, the board must understand and approve the strategies and instruments used, setting appropriate limits for their use. The board needs to ensure that treasury has not sacrificed long-term flexibility or survival for short-term gain, especially in view of the current financial markets situation.

4.7.2 The board must examine the company's activities and structure to determine the types of risks to which it is exposed. It should estimate the size of these exposure risks, providing an indicator as to their importance to the overall operations and financial performance of the company.

4.8 Other policy areas

4.8.1 Other common areas that need to be approved by the board on an ad hoc basis include:

(a) financing major projects (domestic and international)

(b) performance bonds and guarantees

(c) off-balance-sheet financing

(d) acquisitions and sales of assets and liabilities

(e) controls and performance measurement

Examination Style Questions

Question 1 (10 marks – approximately 18 minutes)

In a recent internal audit exercise, the audit manager reported the following findings on the treasury department to the Audit Committee:

(a) There is no mechanism to ensure the foreign exchange transactions and interest rate transactions are carried out at favourable rates;

(b) The dealing records on two transactions were missing; and

(c) 60% of the outstanding transactions were with a bank with BBB credit rating.

Knowing that you are a consultant in treasury management, the CFO of the company has approached you for the directions (ie relating to (a), (b) and (c)) that he should give to the treasury department so as to strengthen the internal controls for weaknesses identified by the internal auditor. (10 marks)

(HKICPA Module B May 2008 Q6)

Question 2 – Inter-company fund transfers

Grow Fast is a multi-national company with 24 group companies located in Europe and the US. Due to inter-company transactions, many of the group companies often make payments to each other by electronic fund transfers each month. Recently, the banks have raised the fee for each transfer by 20% to cover their increasing operating costs. The finance manager of Grow Fast, Tim Macoy, was asked by the CFO to review the costs related to these inter-company fund transfers. Tim has gathered the following data:

Group companies required to make inter-company fund transfers |

24 |

Average number of transfers that each group company makes to every other firm per month |

40 |

Transaction fee charged by the banks for each fund transfer |

HK$100 |

Required:

(a) How much does Grow Fast incur each month on making the inter-company fund transfers? (3 marks)

(b) Explain a technique that Grow Fast can adopt to reduce the number of fund transfers between the group companies without the need for any change in the number of inter-company transactions? (3 marks)

(c) What will the cost of fund transfers to Grow Fast be if it adopts the above technique?

(2 marks)

(HKICPA Module B December 2010 Q7)

Source: https://hkiaatevening.yolasite.com/resources/QPMBNotes/Ch15-Treasury.doc

Web site to visit: https://hkiaatevening.yolasite.com

Author of the text: indicated on the source document of the above text

If you are the author of the text above and you not agree to share your knowledge for teaching, research, scholarship (for fair use as indicated in the United States copyrigh low) please send us an e-mail and we will remove your text quickly. Fair use is a limitation and exception to the exclusive right granted by copyright law to the author of a creative work. In United States copyright law, fair use is a doctrine that permits limited use of copyrighted material without acquiring permission from the rights holders. Examples of fair use include commentary, search engines, criticism, news reporting, research, teaching, library archiving and scholarship. It provides for the legal, unlicensed citation or incorporation of copyrighted material in another author's work under a four-factor balancing test. (source: http://en.wikipedia.org/wiki/Fair_use)

The information of medicine and health contained in the site are of a general nature and purpose which is purely informative and for this reason may not replace in any case, the council of a doctor or a qualified entity legally to the profession.

The texts are the property of their respective authors and we thank them for giving us the opportunity to share for free to students, teachers and users of the Web their texts will used only for illustrative educational and scientific purposes only.

All the information in our site are given for nonprofit educational purposes